Maple has originated $22.3B in loans to date and manages $3.9B in assets under management, bringing institutional-grade credit onchain. Maple Institutional Secured Lending, one of its core products, provides overcollateralized loans to vetted institutional borrowers: stable, secured yield with collateral you can verify onchain. As yields across DeFi have compressed, demand from institutional lenders for dependable, collateral-backed returns has continued to grow.

The growth and performance of Maple Institutional Secured Lending have been strong, but how does it compare to other offerings in the DeFi ecosystem? Aave is the natural place to start.

What the Data Shows

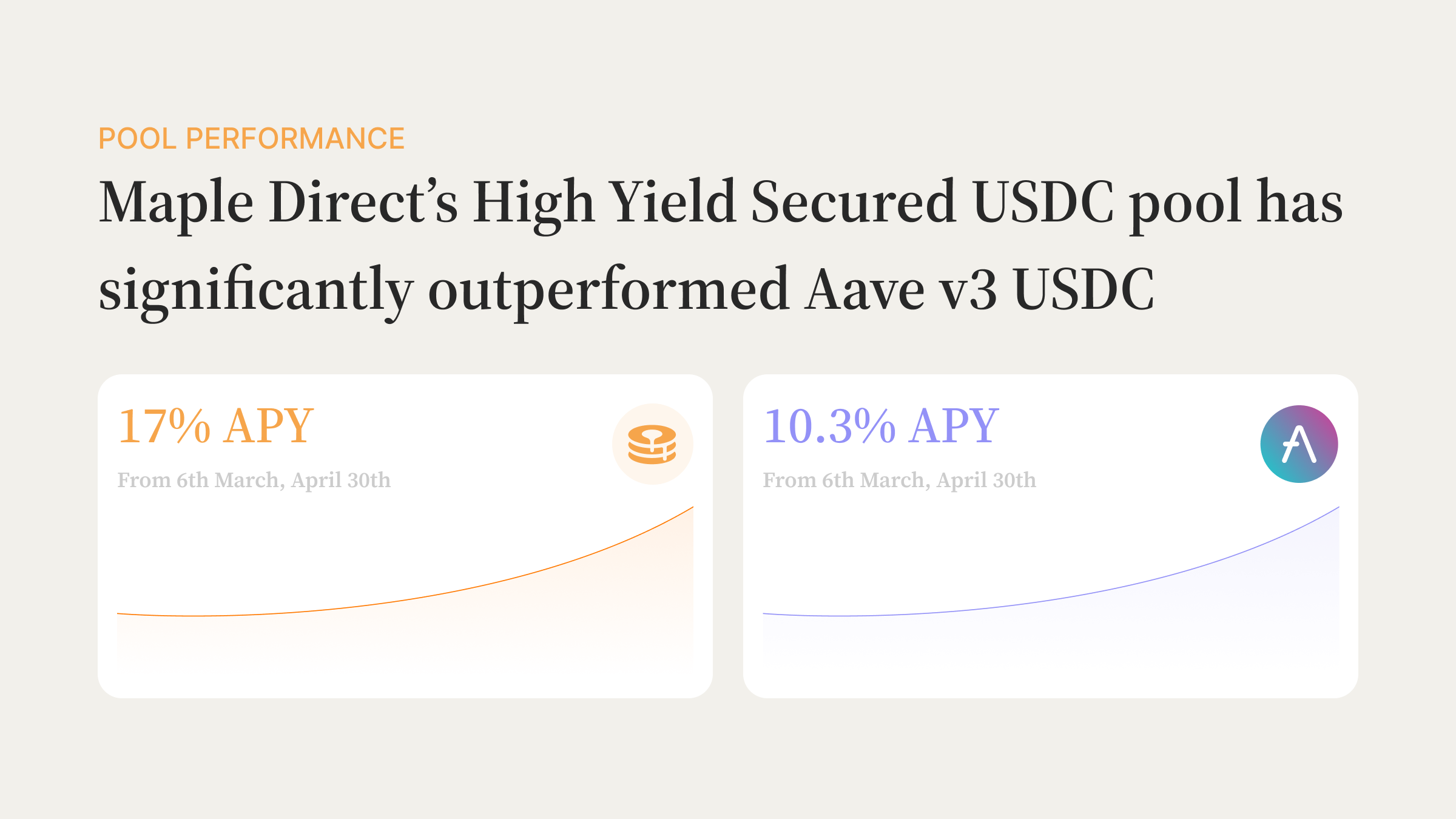

Aave v3 is widely viewed as the base rate for stablecoins in DeFi, and a natural reference point. Both Aave and Maple Institutional Secured Lending bring lenders onchain yield, but they're built differently: Aave is a permissionless, variable-rate money market, while Maple offers secured, overcollateralized lending to vetted institutional borrowers.

Note: this chart reflects metrics as of May 2024, when the article was first published. For the latest data, see the Maple Dune dashboard: dune.com/maple-finance/maple-finance

On the Maple side, our Pool_v2 smart contracts have a sophisticated accounting system where the Pool’s total_assets is comprised of idle cash, outstanding loans, and all accrued interest. This value is used to find the Pool’s current exchange rate for every share (i.e. the amount of $ that each share, or LP token, is currently worth). This is as precise as it gets! And the steady increases of exchange rate over time, based on the issuance rate of the underlying loan contracts, results in the stable yield seen in our pool.

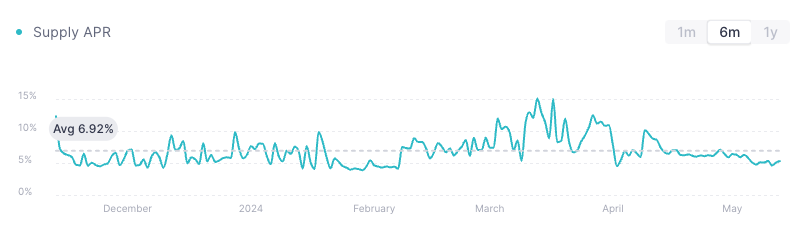

On the Aave side, the supply rate fluctuates based on borrow utilization in each pool (among other factors, including the proportion of borrows that are stable / variable, the reserve factor, etc.). Suffice it to say, this can lead to variable returns for lenders over time. We quantified this by using the ReserveDataUpdated event, which is fired when the supply rate changes (e.g. upon deposit of USDC into the pool). By taking an average of all updates to the supply rate on each day, and converting to APY, we can back into a rough daily yield on the supply side historically. The number is slightly higher than Aave’s frontend display, but directionally correct. Take a look at the chart from the last 6 months in the v3 USDC pool.

Aave supply rates (APR) have averaged just under 7% over the past 6 months (source)

Note: this chart reflects metrics as of May 2024, when the article was first published. For the latest data, see the Maple Dune dashboard: dune.com/maple-finance/maple-finance

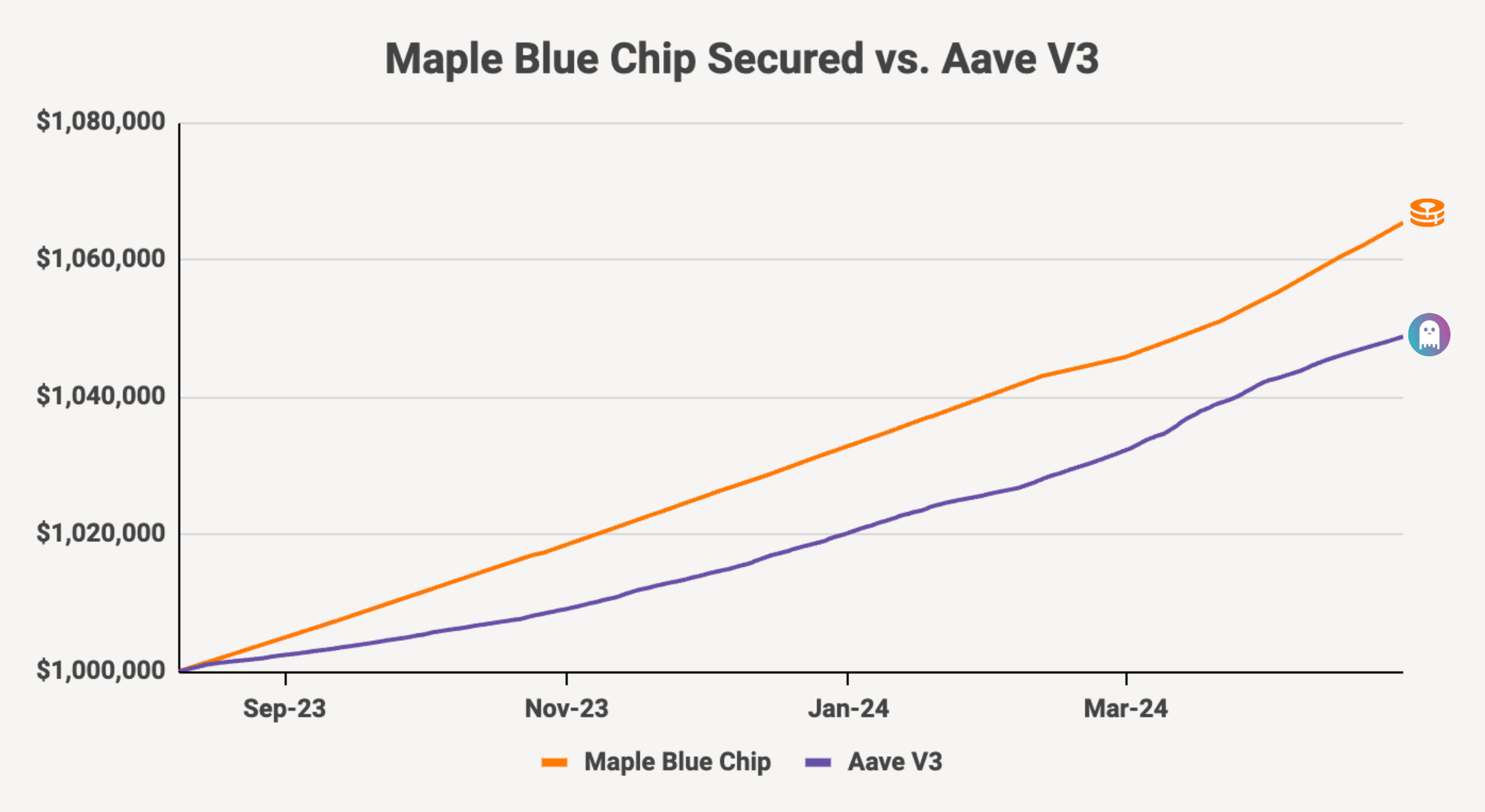

Over time, that structure smooths out the swings a variable-rate market sees. Maple's secured lending is built for stable, collateral-backed yield, while Aave's rate floats with utilization. The chart above compares the two over the original period (see the date note); for current figures, the Maple Dune dashboard is the live source.

Growth of a 1MM USDC deposit since inception in August 2023.

Note: this chart reflects metrics as of May 2024, when the article was first published. For the latest data, see the Maple Dune dashboard: dune.com/maple-finance/maple-finance

Final Thoughts

Maple Institutional Secured Lending has built a track record of stable, collateral-backed yield, but there are other considerations from a lender's perspective when deciding where to park capital. It offers structural differences from Aave that can give institutional lenders additional comfort.

- KYC'd borrowers provide peace of mind that the other side of the pool is a reputable, fully institutional firm that has gone through a full, comprehensive underwrite.

- Furthermore, knowing the borrowers provides additional avenues for potential recourse (beyond posted collateral) in the event of default.

- Specific loans in the pool are transparently displayed with the collateral posted by the borrower for each loan; all loans are overcollateralized, with collateral coverage shown live per loan.

- Collateral is limited to high-quality, liquid digital assets, accepted only after a thorough review.

- Legal structure for the lender whereby their lending position is governed by legal documentation.

And lastly, many of our lenders value the white-glove service and direct, 24/7 communication channel with the Maple team. The aim is always an exceptional lender experience, one we keep working to improve.

Explore Maple Institutional Secured Lending here:

Joe Flanagan

Chairman and Co-Founder

Joe Flanagan is the Co-Founder and Executive Chairman at Maple. Joe is responsible for Maple's overall strategy and growth.